Adjust a linear model with lasso regularization, that is a (possibly weighted) \(\ell_1\)-norm. The solution path is computed at a grid of values for the \(\ell_1\)-penalty. See details for the criterion optimized.

Arguments

- x

matrix of features, possibly sparsely encoded (experimental). Do NOT include intercept. When normalized os

TRUE, coefficients will then be rescaled to the original scale.- y

response vector.

- lambda1

sequence of decreasing \(\ell_1\)-penalty levels. If

NULL(the default), a vector is generated withnlambda1entries, starting from a guessed levellambda1.maxwhere only the intercept is included, then shrunken tominratio*lambda1.max.- penscale

vector with real positive values that weight the \(\ell_1\)-penalty of each feature. Default set all weights to 1.

- intercept

logical; indicates if an intercept should be included in the model. Default is

TRUE.- normalize

logical; indicates if variables should be normalized to have unit L2 norm before fitting. Default is

TRUE.- refit

logical: indicates if the non null coefficients should be refit to avoid excessive bias. Default is FALSE. Can be changed later (both raw and refit coefficients are stored).

- nlambda1

integer that indicates the number of values to put in the

lambda1vector. Ignored iflambda1is provided.- minratio

minimal value of \(\ell_1\)-part of the penalty that will be tried, as a fraction of the maximal

lambda1value. A too small value might lead to instability at the end of the solution path corresponding to smalllambda1combined with \(\lambda_2=0\). The default value tries to avoid this, adapting to the '\(n<p\)' context. Ignored iflambda1is provided.- maxfeat

integer; limits the number of features ever to enter the model; i.e., non-zero coefficients for the Elastic-net: the algorithm stops if this number is exceeded and

lambda1is cut at the corresponding level. Default ismin(nrow(x),ncol(x))for smalllambda2(<0.01) andmin(4*nrow(x),ncol(x))otherwise. Use with care, as it considerably changes the computation time.- beta0

a starting point for the vector of parameter. By default, will initialized zero. May save time in some situation.

- control

list of argument controlling low level options of the algorithm –use with care and at your own risk– :

verbose: integer; activate verbose mode –this one is not too risky!– set to0for no output;1for warnings only, and2for tracing the whole progression. Default is1. Automatically set to0when the method is embedded within cross-validation or stability selection.timer: logical; use to record the timing of the algorithm. Default isFALSE.maxiterthe maximal number of iteration used to solve the problem for a given value of lambda1. Default is 500.methoda string for the underlying solver used. Either"quadra","fista"or"pgd". Default is"quadra".thresholda threshold for convergence. The algorithm stops when the optimality conditions are fulfill up to this threshold. Default is1e-7for"quadra"and1e-2for the first order methods.monitorindicates if a monitoring of the convergence should be recorded, by computing a lower bound between the current solution and the optimum: when'0'(the default), no monitoring is provided; when'1', the bound derived in Grandvalet et al. is computed; when'>1', the Fenchel duality gap is computed along the algorithm.

Value

an object with class QuadrupenFit.

an object with class ElasticNetFit, inheriting from QuadrupenFit.

Note

The optimized criterion is the following:

penscale argument.

Examples

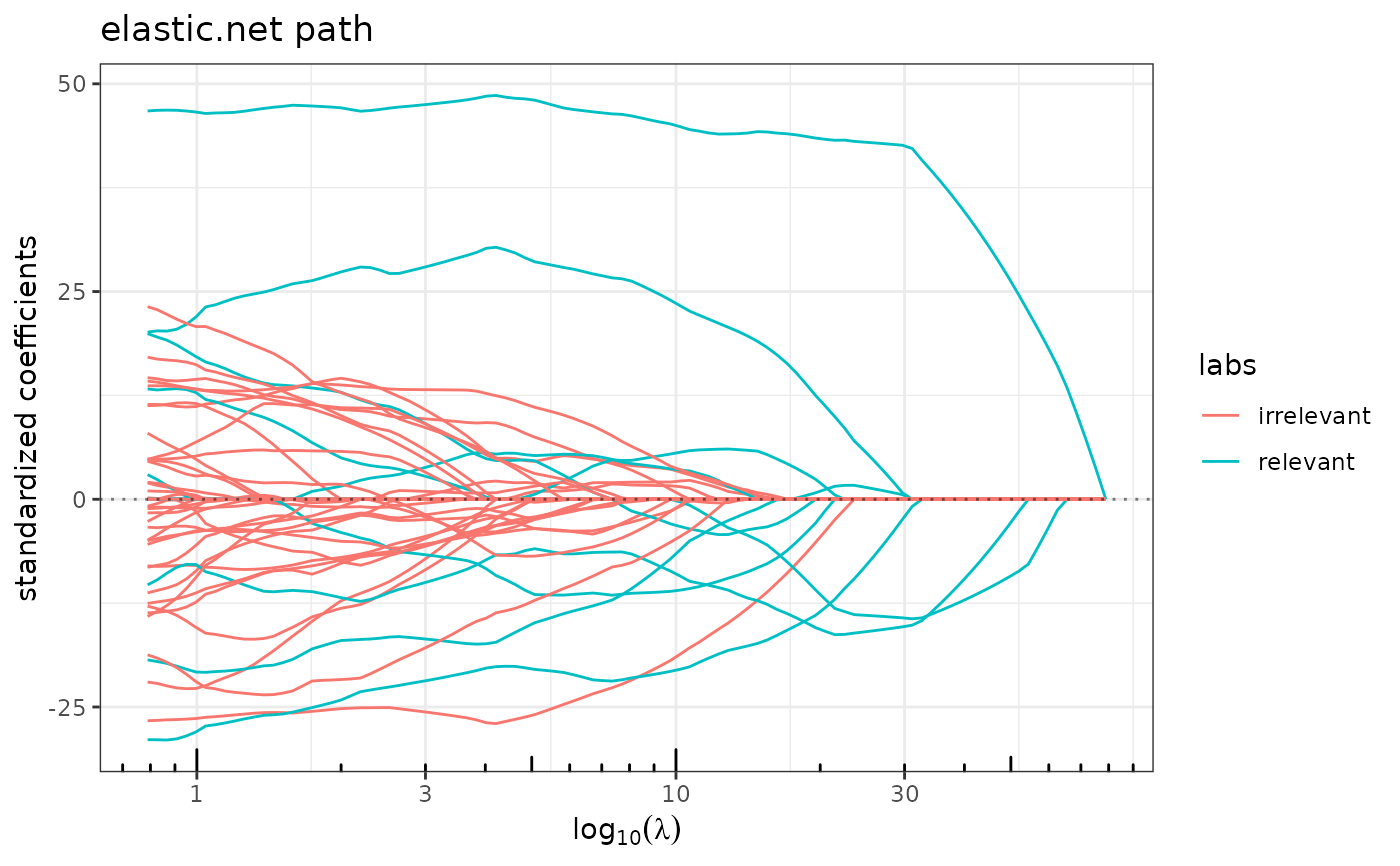

## Simulating multivariate Gaussian with blockwise correlation

## and piecewise constant vector of parameters

beta <- rep(c(0,1,0,-1,0), c(25,10,25,10,25))

cor <- 0.75

Soo <- toeplitz(cor^(0:(25-1))) ## Toeplitz correlation for irrelevant variables

Sww <- matrix(cor,10,10) ## bloc correlation between active variables

Sigma <- Matrix::bdiag(Soo,Sww,Soo,Sww,Soo)

diag(Sigma) <- 1

n <- 50

x <- as.matrix(matrix(rnorm(95*n),n,95) %*% chol(Sigma))

y <- 10 + x %*% beta + rnorm(n,0,10)

labels <- rep("irrelevant", length(beta))

labels[beta != 0] <- "relevant"

## The solution path of the LASSO

plot(lasso(x,y), label=labels)